Today Apple made some big announcements. First, the new iPhones, dubbed iPhone 6 (4.7″) and iPhone 6 Plus (5.5″), featuring a completely new design that resembles the original iPhone. Then, the company revealed its new NFC-based payments system, called Apple Pay. And lastly, the super-hyped Apple Watch. Here are my opinions about the announcements.

iPhone 6 and iPhone 6 Plus

As you can see on the photo above, the design is totally new and, in fact, resembles the original iPhone a lot. A quick summary of what you need to know:

- There are two sizes now: 4.7″(iPhone 6) and 5.5″ (iPhone 6 Plus). To give you an idea of the new sizes, the iPhone 6 is about the size of the Google Nexus 5

, and the iPhone 6 Plus is very close to the Samsung Galaxy Note 4

.

- Retina HD displays on both models, with a 1334×750 resolution on the iPhone 6, and a 1920×1080 resolution on the iPhone 6 Plus.

- Landscape view on the iPhone 6 Plus.

- New processor on both: 64-bit A8 processor and M8 motion co-processor.

- New 8-megapixel iSight camera, with a 5-element f/2.2 lens and 1/1.8″ sensor. Optical image stabilization available on the iPhone 6 Plus. It shoots 1080p video at 60 fps and 720p at 240 fps.

- New 1.2-megapixel Facetime camera, with a f/2.2 lens and backside illuminated sensor, capable of recording 720p video .

- Real LTE world phone, with support for up to 20 bands.

- 802.11ac WiFi, the newest, fastest standard.

- NFC for payments using Apple Pay (see below).

- Includes Touch ID, of course.

- Comes with iOS 8.

The new iPhones look good and are an evolution over the Apple iPhone 5s. The two important new features are Apple Pay and (almost) worldwide LTE support, which helps us international travelers. I will discuss Apple Pay in a second.

Design-wise, although they look really great, I think the footprint is too big, making both phones bigger than competitors with larger screen sizes. Examples:

- iPhone 6 (4.7″ display, dimensions of 5.44 x 2.64 x 0.27 inches) vs Google Nexus 5 (5.0″ display, dimensions of 5.43 x 2.72 x 0.34 inches)

- iPhone 6 Plus (5.5″ display, dimensions of 6.22 x 3.06 x 0.28 inches) vs Samsung Galaxy Note 4 (5.7″ display, dimensions of 6.04 x 3.09 x 0.33 inches).

I am not sure I am ready to carry a Note 4-sized iPhone in my pocket, even though the landscape UI looks great on the iPhone 6 Plus. I am going to wait and see both models at the Apple Store before making a purchase decision.

I will review this phone and iOS 8 once they are released, so come back for more later.

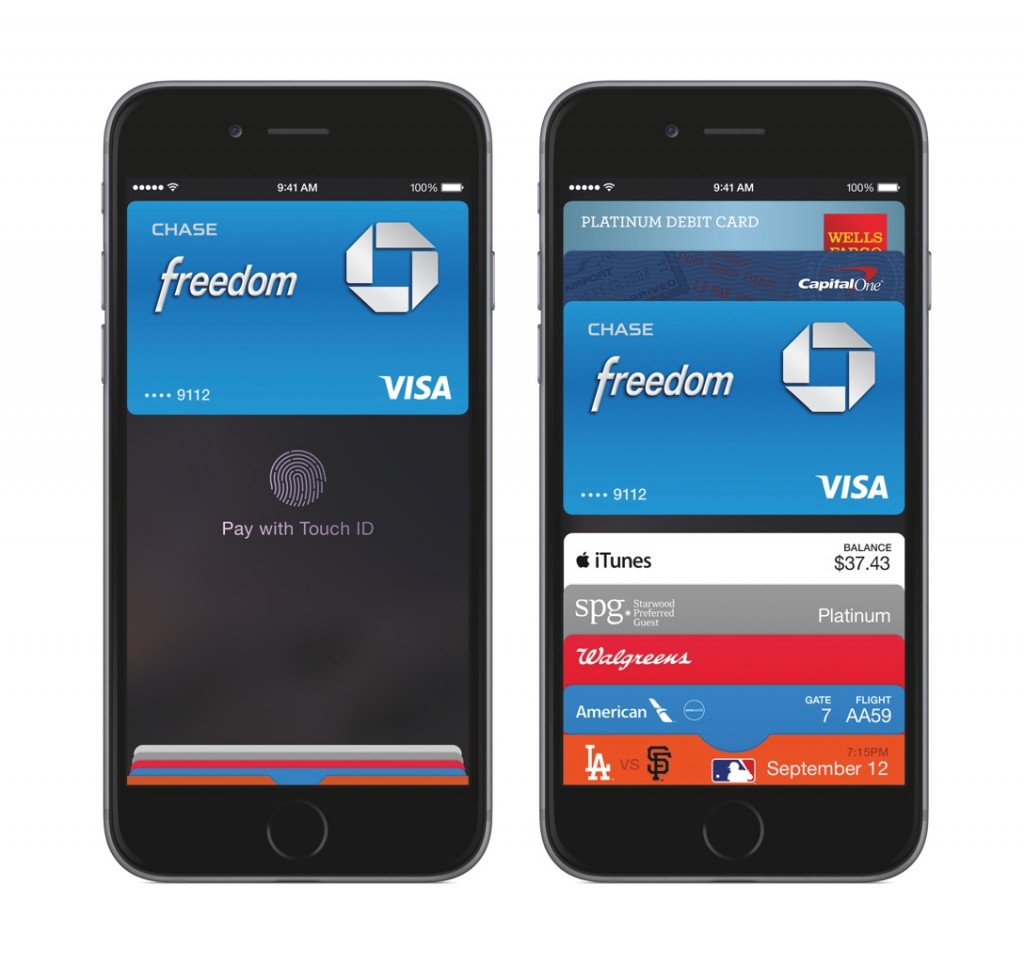

Apple Pay

Probably the most important announcement made today. A long time ago, when Google started demonstrating its Google Wallet, I told someone on Facebook (or Twitter, can’t remember) that mobile payments would not take off until Apple hits the field. At the time, this kind of comment was seen as blind fanboyism, but proved right. One thing that Apple is great at is dragging partners into its crazy endeavours — iTunes Store, Apple TV, iBookstore, Newsstand, Passbook, you name it. The mobile payment stuff is no exception. At launch (actually in October, U.S. only), it already has onboard the 3 largest credit card companies (Visa, Mastercard and American Express), 10 major banks and 220000+ stores, plus 10 apps for online shopping.

You may be asking why Apple Pay might work, where many others have failed. To start, the initial ecosystem is already huge:

- Current financial partners account for 83% of all credit card purchase volume in the U.S..

- Current retailers are the largest in their fields: department stores (Macy’s and Bloomingdale’s), drug stores (Walgreens and Duane Reade), restaurant chains (Subway and McDonald’s), and so on.

Second, implementation. Instead of being just a credit card number storage, with verification numbers, PIN codes and all the nuisances, Apple Pay creates a new implementation that is both secure, private and easier to use than current methods. First, the technology:

- It uses NFC (near-field communications), which is embedded into all iPhone 6 and iPhone 6 Plus devices. Some may joke and welcome Apple to 2011, but NFC has been borderline useless so far, without an ecosystem to drive its wide adoption. NFC is more secure than, let’s say, Bluetooth 4.0 LE, since its harder to intercept the signal (long range vs. very short range).

- Apple has the only fingerprint reader in the market that works properly, Touch ID, which many of you are already using on the iPhone 5S to unlock your phone and make purchases at the App Store.

- Apple already has Passbook, a convenient way of storing all sorts of cards, that you may already used at the airport boarding gate or Starbucks.

- An isolated chip called the Secure Element keeps the payment data encrypted and isolated from the rest of the device. As far as I could investigate, there is no API to allow access to your payment data directly (i.e. not via Apple Pay).

- Find My iPhone helps dealing with lost or stolen devices.

So, how does it work? First, you need a credit card in Passbook. You may add your card from your iTunes Account, or add a new card. Adding a new card is very easy:

- You will be requested to take a picture of the front of the card.

- Then you will be asked to go to your bank to confirm that the card is really yours. After that, the card is added to Passbook.

- After that, you will be able to Pay using that card on Passbook via a fingerprint confirmation using Touch ID.

If you are wondered about security and privacy, here is how it works:

- Credit card numbers are not stored in the device and are never transmitted to the merchant.

- A device-only account number is created to represent your credit card and is stored in the Secure Element.

- Every time you make a payment, a one-time payment number plus a dynamically generated security code are used for the transaction. So your card number and the security code are not needed to complete a transaction and the merchant will never know your name or credit card information.

- In case you lose your device, you may use Find My iPhone to suspend all payments from that device. Since the credit card number is not stored in the device, you don’t need to cancel your credit card.

- Apple doesn’t collect information on the purchase. The transaction happens only between you, the merchant and your bank.

I am eager to see how this gets traction in the U.S. and worldwide. With a good implementation and that sort of starting partners, it’s worth keeping an eye on Apple Pay in the near future.

One more thing… the Apple Watch

Tim Cook showed us “one more thing…” for the first time. And it was the over-hyped iWatch, which is officially called the Apple Watch. Before I start talking about it, full disclosure first: I am not a smartwatch enthusiast. I am an old school guy who like mechanical swiss timepieces and I can’t find a use for a second screen on my wrist. I wear a watch because I want to, not because I have to. And I can’t find a compelling reason to have to wear a smartwatch. That said, let’s start.

The Apple Watch follows along some lines drawn by competitors like Samsung, LG and Motorola. The smartwatch has a LCD display that shows you information and can run some apps. That’s where similarities stop.

The Apple Watch comes in 3 variants and two sizes (38mm and 42mm):

- WATCH: stainless steel case, sapphire glass and several band options.

- WATCH SPORT: anodized aluminum case, Ion-X glass and several colorful band options.

- WATCH EDITION: 18K gold cases, sapphire glass and several band options.

Design-wise, it will appeal to some geeks and fashionistas. I personally don’t like it. I think it is too geeky and too big. The UI borrows the good old crown to act as a digital input wheel. This is where Apple got it right — design is not about how it looks, but how it works. And the UI seems to work much better than in the other smartwatches I tried.

The Apple Watch features are very similar to the other Android smartwatches: messages, tweet notifications, maps, weather, etc. A nice touch was adding Apple Pay to the watch. Continuity is also available, but I doubt any sane people will start reading emails on the Apple Watch and continue on the iPhone. The heart-rate monitor uses a sensor that is very clever and cool. Clearly Apple has thought deeply about this being a health and fitness device. Lastly, Mag Safe technology plus inductive charging avoid the use of an ugly connector to charge the device.

The Apple Watch comes in early 2015 and the price starts at $349. It is priced accordingly to its competitors, but too expensive for a watch. Nevertheless, younger people don’t wear watches. Maybe this will appeal to them.

As a final comment, the Apple Watch does scream “First generation Apple product”. It is not very polished (too big and the design is weird), it still requires an iPhone to work and people still don’t know what to do with it. In some aspects, it reminds me the first iPad. It was big, cumbersome, expensive and people didn’t know why they should buy one. Four years later, it is the undisputable champion in the tablet market. I wonder if the same is going to happen with the Apple Watch. Let’s wait for it and see.

You can watch the keynote at the Apple website.

* all photos belong to Apple Inc.. Used with permission.